India’s GDP (gross domestic product) grew 7.6% in 2QFY09 (Jul-Sep ’08), in line with our estimate and ahead of consensus (7.2%).

There has been a slowdown in all the major components: agriculture (2.7%), manufacturing (6.1%) and services (9.6%). The deceleration, however, has been much more modest than what was envisaged by the Street. The growth in 1HFY09 at 7.8%.

In line with liquidity and credit problems faced in recent months, we expect GDP growth to slow in 3QFY09 to around 7.2%. The trend is likely to reverse in 4QFY09 and projected to be 7.8% in FY09. The performance of agriculture, mining, electricity and personal and social services are likely to improve in 2HFY09, while manufacturing, construction and trade, hotel, transport and communication are likely to witness deceleration.

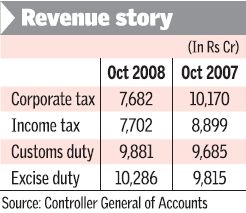

Tax Revenues Decline in Oct-2008: