Merill Lynch has raised the stock target price of Reliance Capital [R-Cap] to Rs 1850. R-Cap is expanding its distribution at a very rapid pace which could result in growth, ahead of Merill’s estimates, remaining very strong through FY10 and possibly beyond. Based on FY10E sum of parts valuation, a value of Rs 2033/share, the target price for Mar’09 (18 months from now), a 36% upside. Hence, 12 month PO is Rs 1850.

Merill Lynch has raised the stock target price of Reliance Capital [R-Cap] to Rs 1850. R-Cap is expanding its distribution at a very rapid pace which could result in growth, ahead of Merill’s estimates, remaining very strong through FY10 and possibly beyond. Based on FY10E sum of parts valuation, a value of Rs 2033/share, the target price for Mar’09 (18 months from now), a 36% upside. Hence, 12 month PO is Rs 1850.

By Dec’08, it is likely to have 10,000 touch points in retail in 1 year (v/s 4,000 now), 5,000 locations (v/s 700), 300,000 agents in life insurance (and 400 cities) and +1500 dealers.

- Consumer loan book [Housing, Auto, Personal etc] to expand 10-fold to US$4.1bn by FY10, delivering ROE of +20%.

- General insurance too is likely to show +100% growth through FY09 and 75% in FY10.

- R-Money is likely to be the other strong growth driver as it expands distribution and customers hit 1 million mark.

- Overall, life insurance should, however, remain the biggest contributor at 37% of target value with premia income forecast to rise 7-fold from FY07 levels.

Reliance Capital is likely to emerge amongst the top 3-4 players in the financial services segment. R-Cap is expected to report an EPS of Rs 41.16 for FY 08 and Rs 59.27 for FY09.

In a separate report, Merill Lynch’s most preferred stocks are – BHEL, Bharti Airtel and Grasim Industries. While the least preferred are Hindalco, Tata Motors and Pantaloon Retail India Ltd.

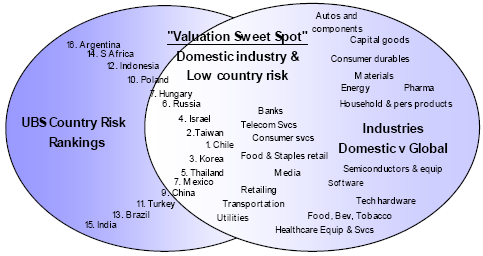

Rank of India across various parameters in the UBS Report are as follows, [1=Highest Score, 16=Lowest Score]

Rank of India across various parameters in the UBS Report are as follows, [1=Highest Score, 16=Lowest Score]