Punj Lloyd (PLL) announced its consolidated results; revenue was up 54% at INR29.5bn (our estimate was INR25.9bn, consensus estimate INR26.2bn). Net profit was up 61% to INR1.44bn (our estimate INR0.84bn, consensus INR1.1bn). A large part of the order inflow of INR56bn in 2QFY09 was driven by the INR36.4bn EPC order by Qatar Petroleum.

Management continues to be confident given the robust backlog of Rs217bn (1.9x FY09E sales). The company has minimal exposure to real estate and most of the clients are government companies.

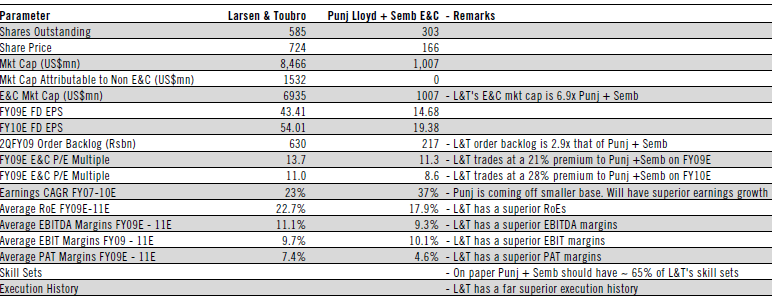

Punj is the only Indian E&C company that can give L&T a run for its money; Acquisition of Semb E&C has helped scale up expertise; Punj has moved up the value chain: order size increasing from US$30mn to US$100mn (FY07) to US$150mn (FY08) – Recent US$800mn Qatar order being case in point.

Punj Lloyd is expected to report an EPS of Rs 14.5 and Rs 19.5 for FY09 and FY10 respectively.

Punj Lloyd Versus L&T: [Expandable Image] Courtesy: Citigroup Research

Courtesy: Citigroup Research

We personally place our investment bets on Punj Lloyd rather than L&T with the same logic as betting on a horse which has already won in comparison to the horse which is ready to win and hit a jack pot.